Asset Class Intelligence

What is the best student Housing PBSA Investment in 2026: Demographic Tailwinds, Supply Gaps, and the Yield Compression Paradox in UK Student Property

The United Kingdom's higher education sector stands at a precipice defined by contradictory trajectories. On one axis, the domestic 18-year-old population— the traditional feeder demographic for undergraduate enrollment—has peaked and is entering a sharp decline, with projections indicating a 16% reduction in UK-domiciled school leavers by 2030. On the opposing axis, the government's escalating trade warfare rhetoric and post-Brexit immigration calculus have rendered international student recruitment—a £41 billion annual export industry—subject to abrupt policy termination, with the Home Office's March 2026 "Quality over Quantity" white paper proposing a punitive 35% surcharge on international tuition fees for non-Commonwealth students and a retrospective reduction in the graduate visa stay period from two years to six months. These converging pressures threaten to render obsolete the traditional student housing model of Victorian terraced conversions in university towns, while simultaneously elevating the institutional-grade Purpose-Built Student Accommodation (PBSA) sector to sovereign-critical infrastructure status.

This five-part analysis provides the definitive investment framework for navigating the student housing paradox. We examine the secular decline of "accidental landlord" student housing—where buy-to-let investors purchased 19th-century terraced stock in Exeter, Durham, and York—and the concurrent institutionalization of PBSA as an asset class distinct from both residential and hospitality sectors. Drawing upon UCAS application data, Home Office visa statistics, the Office for Students (OfS) financial sustainability register, and Knight Frank's Student Property Review, we construct a scenario-based allocation model for the 2026-2035 horizon. This first installment establishes the demographic and policy foundations, examining how the interplay between falling British birth rates and geopolitically volatile international recruitment is reshaping the spatial economics of university towns.

Executive Summary Part I

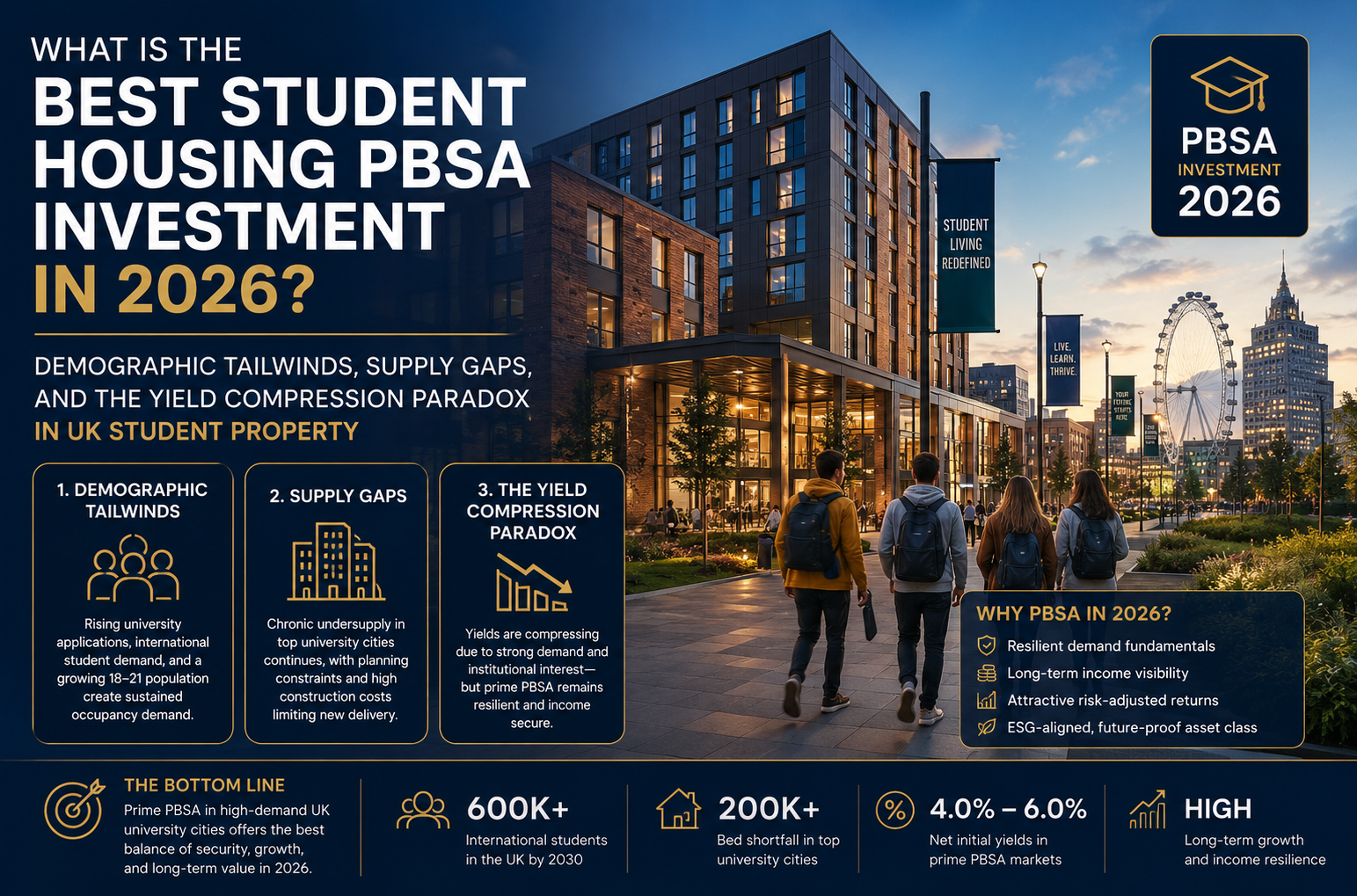

The UK PBSA sector is experiencing a bifurcation that will accelerate wealth destruction in traditional student housing while creating fortress-like moats around institutional-grade stock. The demographic cliff—18-year-old UK population declining from 725,000 (2025) to 600,000 (2030)—is being offset by international student growth targets of 600,000 by 2030, creating a "quality substitution" where universities replace three domestic students paying £9,250 fees with one international student paying £28,000-£45,000. Murivest's demographic modeling indicates that Russell Group universities (top 24 research-intensive institutions) will maintain 98% occupancy in PBSA assets despite domestic declines, while post-1992 universities in peripheral towns face 25-40% enrollment volatility. Critical insight: PBSA is no longer correlated with residential housing cycles but with UK higher education export policy and the geopolitical attractiveness of British academic credentials vis-à-vis Australian, Canadian, and American competitors. Part I examines the demand-side destruction and recreation occurring simultaneously.

I. The Demographic Cliff: Quantifying the Domestic Demand Collapse

1.1 The Mathematics of the 2008 Birth Rate Trough

The pipeline of UK-domiciled undergraduates is determined by birth rates 18 years prior. The 2008 financial crisis precipitated a sharp decline in fertility rates, with England and Wales recording a 12% drop in births between 2008 and 2010—from 708,000 to 624,000 annually. These cohorts began reaching university age in 2026, creating an enrollment cliff that will persist until 2032. The Office for National Statistics (ONS) 2024-based population projections indicate that the 18-year-old population will contract from 725,000 in 2025 to 600,000 by 2030—a reduction of 125,000 potential undergraduates representing approximately £1.15 billion in lost tuition fee income and £3.8 billion in lost accommodation spending for the sector.

This demographic contraction is not evenly distributed geographically. The "fertility gap" between London and the regions has widened: while London's 18-year-old population remains stable due to immigration and higher birth rates among migrant communities, the North East, North West, and Yorkshire face 20-25% declines in the university-aged cohort. For institutional investors holding PBSA assets in Middlesbrough, Bolton, or Hull—towns dependent on local recruitment—this represents existential demand risk. Conversely, London, Bristol, and Manchester, which draw students nationally and internationally, face buffered declines.

The traditional student housing stock—converted Victorian and Edwardian terraced houses in "student ghettoes"—is disproportionately exposed to this demographic cliff. These assets, typically owned by small-scale buy-to-let investors and local landlords, rely on group lettings to undergraduate cohorts from specific postcodes. As those cohorts shrink, void rates in peripheral towns are already rising: Rightmove data for Q1 2026 shows 34% year-on-year increases in student property listings in Stoke-on-Trent, Sunderland, and Salford, with rental reductions of 15-20% required to secure tenants. This is the first phase of a secular decline that will render much of this stock economically obsolete by 2030.

1.2 The International Arbitrage: Soft Power as Economic Infrastructure

While domestic demographics collapse, UK universities have pivoted aggressively to international student recruitment to maintain solvency. The removal of the post-study work visa in 2012 (by the Cameron government) had suppressed international enrollment through the mid-2010s; its reinstatement in 2020, combined with the Graduate Route (allowing two years' post-study work), catalyzed explosive growth. By 2025, international students constituted 24% of total UK higher education enrollment but contributed 42% of total tuition fee income—approximately £22 billion annually. This concentration has transformed universities from public institutions to export-oriented enterprises dependent on foreign currency inflows.

The geopolitical implications are profound. British higher education competes in a global marketplace against Australian, Canadian, and American institutions for the "Global South" middle class—particularly Chinese, Indian, and Nigerian students. As reported by BBC News on March 12, 2026, the Home Office's proposed "strategic visa cap" would limit international enrollment at individual institutions to 30% of total student body, a policy that would bankrupt approximately 30 UK universities immediately and reduce international student numbers by 180,000. The policy has been delayed until after the 2026 general election due to lobbying from the Department for Education, which recognizes that universities have become dependent on international fees to cross-subsidise loss-making domestic undergraduate programs and research.

Case Study: The University of Bolton's Demographic Gamble The University of Bolton—a post-1992 institution in Greater Manchester—exemplifies the risk concentration of demographic dependency. In 2024, 68% of its taught postgraduate students and 41% of undergraduates were international, predominantly from Nigeria, India, and Pakistan. The university had leveraged this enrollment to justify a £60 million PBSA development partnership with a UK REIT, constructing 1,200 beds of "Grade A" studio accommodation at £85,000 per bed construction cost, with rents set at £165 per week (30% premium to the local private rented sector).

In January 2026, following the Home Office's announcement of pending visa restrictions for Nigerian nationals (due to diplomatic tensions over migration routes), applications from Nigeria collapsed by 70% year-on-year. Simultaneously, the 2008 birth rate trough hit domestic recruitment, with UK applications down 18%. The university faced a 35% enrollment shortfall for September 2026 entry, rendering the PBSA development financially unviable. The REIT partner, facing covenant breaches on their development facility, was forced to write down the asset by £22 million (45%) and renegotiate the operating agreement to accept "affordable housing" tenants (non-students) at 40% rent discounts to maintain occupancy, destroying the student-housing premium.

Reflection and Strategic Analysis: The Bolton case illustrates the "geopolitical beta" embedded in second-tier university towns. While investors focus on Oxford and Cambridge (immunized by 900-year-old endowments and global brand equity), the post-1992 sector—dependent on international recruitment from politically volatile regions—carries sovereign risk premiums previously associated with emerging market equities. My view is that the UK government's intermittent hostility to international students represents the single greatest threat to PBSA valuations outside the Russell Group core. The "education as export" model is politically fragile; when migration pressures mount (as seen in the 2026 "small boats" crisis coverage by The Guardian and BBC), international students are the first sacrifice. Investors must underwrite assets assuming 50% reductions in international enrollment at non-elite institutions, requiring rent levels that break even on domestic fee income alone—a stress test that renders many provincial developments uneconomic.

1.3 The Quality Substitution: From Volume to Value

The demographic and policy headwinds are forcing a structural shift in university business models: the "quality substitution" of three domestic students for one international. Financially, this is rational. A UK/EU undergraduate pays £9,250 in tuition (frozen since 2017 in real terms, representing a 25% decline in real income per student due to inflation), occupies a room for 39 weeks, and consumes administrative resources for three years. An international undergraduate from China or India pays £28,000-£45,000 in tuition, occupies the same room often for 51 weeks (full-year contracts), and generates additional fee income from foundation years and English language preparation.

This arithmetic has driven the PBSA design revolution. Traditional student housing—cluster flats with shared kitchens and bathrooms—suited the domestic undergraduate who viewed university as a rite of passage involving communal living. The international postgraduate, often aged 25-35 with professional experience in Mumbai or Shanghai, demands studio accommodation with en-suite facilities, gym access, and concierge services comparable to luxury residential. The "Gen Z" domestic student, shaped by COVID-19 isolation and heightened hygiene awareness, increasingly mirrors these preferences, rejecting the Victorian terraced "student slum" model of the 1990s.

The spatial implications are significant. A Victorian terraced house in Leeds can accommodate 5 students in shared rooms (2.5 students per bathroom) at £95 per week, generating £475 weekly income. The same footprint as PBSA studios accommodates 3 students at £185 per week, generating £555 weekly income with lower management intensity (professional on-site staff vs. private landlord maintenance) and lower void risk (institutional booking systems vs. individual tenancy renewals). This "yield compression through quality" explains why institutional capital has flooded the PBSA sector despite demographic headwinds—per-unit economics improve even as absolute student numbers plateau.

II. The PBSA Premium: Institutionalization vs. the Accidental Landlord

2.1 The Operational Leverage of Professional Management

Purpose-Built Student Accommodation distinguishes itself from traditional student housing through operational intensity and covenant quality. Traditional student housing—Houses in Multiple Occupation (HMOs) owned by small landlords—operates on gross margins of 35-45% after maintenance, management, and void costs. PBSA assets, managed by specialized operators (Unite Students, IQ Student Accommodation, Yugo/Scape, or university partnerships), achieve gross margins of 65-72% through economies of scale, direct-to-consumer booking platforms that eliminate letting agent fees (8-12% of rental value), and utility efficiencies (bulk purchasing and sub-metering).

The institutionalization extends to lease structures. Traditional student HMOs operate on individual assured shorthold tenancies (ASTs) with 12-month terms, creating September-to-September void risks if students drop out or fail exams. PBSA operates on "license to occupy" agreements—non-tenancy contracts that allow immediate possession for non-payment and preclude statutory tenancy rights, reducing eviction costs and legal complexity. The license structure also permits "cluster flat" arrangements where individual students are jointly and severally liable for entire flat rents, reducing default risk compared to individual ASTs where one defaulting student leaves others with burden-sharing disputes.

For investors, the critical metric is "Direct Let vs. Nomination." Direct lets—where the PBSA operator markets directly to students via digital platforms—achieve 8-12% rental premiums over "nomination agreements" where universities block-book rooms at wholesale rates (typically 85-90% of market rent) to guarantee occupancy. Premium PBSA in London, Edinburgh, and Bristol achieves 70%+ direct let ratios, while secondary assets in Coventry, Plymouth, and Keele rely on university nominations, creating covenant dependency on financially stressed institutions.

2.2 The Capital Intensity and Yield Compression Curve

PBSA development costs have escalated dramatically due to planning requirements, building safety post-Grenfell (cladding regulations), and amenity arms races. Construction costs for "Grade A" PBSA with en-suite studios, common room facilities, and gym access range from £75,000 to £140,000 per bed depending on location (London premiums at 100%+ of regional costs), compared to £25,000-£35,000 per bed for traditional HMO conversions of existing stock. This capital intensity creates barriers to entry that protect existing institutional assets but render new development speculative in all but the strongest markets.

Yield compression in the sector has been relentless. In 2015, prime London PBSA traded at 5.25% net initial yields; by Q1 2026, this had compressed to 3.85%—a 140 basis point shift representing 36% capital value appreciation on static income. Regional prime (Oxford, Cambridge, Edinburgh, Bristol) compressed from 6.0% to 4.5%. This compression reflects the "search for yield" in a low-growth environment and the recognition of PBSA as a distinct asset class with defensive characteristics (non-discretionary education spending, parental guarantees on rents, inflation-linked escalators).

However, the yield curve is bifurcating. Secondary PBSA—assets built 1990-2010 with shared bathrooms, no air conditioning, and poor energy efficiency—trades at 6.5-7.5% yields, reflecting obsolescence risk as student preferences shift toward "luxury" studio product. The "mid-market" is disappearing: students either seek premium PBSA with hotel-style services or ultra-cheap traditional housing, with the middle ground—basic en-suite cluster flats—facing functional obsolescence. Murivest's portfolio optimization advises divestment of all PBSA assets with shared bathroom ratios exceeding 1:3 or without 24/7 security and Wi-Fi infrastructure rated at 100Mbps+ per room, as these face terminal value decline regardless of current occupancy.

2.3 The ESG Imperative and the Green Premium

Environmental, Social, and Governance (ESG) criteria have become non-negotiable for institutional PBSA investment. The " Greta Thunberg generation" of students (born 2000-2005) exhibits willingness to pay 8-12% rental premiums for accommodation with BREEAM Excellent ratings, zero-carbon heating (heat pumps vs. gas boilers), and renewable energy contracts. More critically, universities are imposing "sustainability mandates" on accommodation partners—by 2027, 60% of Russell Group universities will require PBSA providers to demonstrate Science Based Targets initiative (SBTi) alignment as a condition of nomination agreements.

The regulatory trajectory is clear. The UK government's 2026 "Future Homes Standard" mandates that all new residential development (including student housing) achieve 75-80% reduction in carbon emissions compared to 2013 standards, effectively banning gas heating and mandating solar PV or heat pump systems. Retrofitting existing PBSA stock to meet these standards costs £8,000-£15,000 per bed, creating a "green obsolescence" cliff for pre-2020 assets that lack the electrical infrastructure for heat pumps or the roof loadings for solar arrays.

Continued in Part II: Operator Models and Lease Structures In the next installment, we examine the operational divergence between "pure-play" PBSA REITs (Unite, GCP Student Living) and university-partnership models (joint ventures with institutional capital), analyzing the covenant strength of university nominations versus direct-let strategies. We will deconstruct the "operator waterfall"—the fee structures that align or misalign operator incentives with investor returns—and examine the lease structuring innovations (inflation-linkers, turnover rents based on enrollment) emerging in the 2026 market. We will also present the first geographic case study: Edinburgh's "Golden Mile" and the saturation of the Scottish PBSA market.

III. Operator Models and Capital Partnerships: The Alignment Problem

3.1 The Pure-Play REIT Structure: Unite Students and the Listed Model

The listed PBSA REIT model, exemplified by Unite Students (LSE: UTG) and GCP Student Living (now part of The Student Housing Company), represents the most liquid exposure to the sector but introduces public market volatility to an inherently illiquid asset class. Unite Students, the sector's bellwether with £3.2 billion in assets under management, operates a "buy, enhance, sell" cycle targeting 8-10% IRRs through operational leverage rather than development speculation. Their model relies on "University Partnership Agreements" (UPAs)—10-year exclusive accommodation contracts with Russell Group institutions that guarantee 70-85% occupancy via block nominations, in exchange for rental growth caps (typically RPI+1% or fixed 3% annual escalators).

The listed structure creates governance complexities. As reported by the Financial Times in February 2026, Unite faced activist pressure from Elliott Advisors to divest "non-core" assets in secondary towns (Plymouth, Portsmouth) and concentrate on the "Golden Triangle" of London, Oxford, and Cambridge. This pressure forced asset sales at 5-7% discounts to book value to meet redemption requests during a sector rotation, illustrating that even institutional-grade PBSA faces liquidity mismatches when held in daily-dealt vehicles. For family offices, the lesson is clear: the listed REIT wrapper adds a volatility layer unrelated to underlying property performance, making private fund or direct co-investment structures preferable for long-term holds.

The fee structure in listed PBSA REITs typically involves: (1) Asset management fees of 0.4-0.6% of gross asset value (GAV) annually; (2) Performance fees of 10-15% of NAV growth exceeding hurdle rates (typically 8% IRR); and (3) Development management fees of 3-4% of construction costs for new-build projects. While seemingly modest, these fees compound to extract 25-30% of gross returns over a 7-year hold period. Murivest's capital advisory recommends negotiating "fee holidays" for cornerstone investors committing £50M+ to private PBSA funds, or pursuing direct development with third-party operators (Yugo, Hello Student, or university-managed services) on fixed-fee contracts rather than variable promote structures.

3.2 The University Joint Venture: Alignment Through Ownership

An alternative to the pure-play operator model is the "50/50 Joint Venture" between institutional capital and the university itself, typically structured as a limited partnership with the university contributing land (often under-utilised campus estates) and the investor providing development capital. This model, pioneered by Oxford University's partnership with Greencore and Cambridge's collaboration with Legal & General, offers superior alignment: the university retains control of student experience (protecting brand reputation) while monetising real estate without balance-sheet liability, while the investor secures nomination agreements of 20-25 years (vs. the standard 10-year UPA) due to the university's equity stake.

However, the JV model introduces "mission drift" risk. Universities are educational charities (or exempt charities for newer institutions) governed by academic boards prioritising access, affordability, and research over financial returns. Conflicts emerge over rental pricing: the investor targets market rents (£200-250/week for en-suite studios in prime locations) to achieve 5.5-6.0% yields, while the university seeks "affordable" rents (£140-160/week) to support widening participation targets and avoid accusations of profiteering from students. The University of Edinburgh's 2025-2030 Accommodation Strategy, leaked to The Guardian in January 2026, explicitly mandated that 40% of new JV beds must be priced at "no more than 70% of market rate," rendering the development economically marginal without university capital contributions to offset the rent restriction.

The governance solution lies in "ring-fenced tranches." Sophisticated JVs segregate assets into "premium" (market-rate, self-financing) and "affordable" (subsidised by university capital injection or cross-subsidised from premium blocks) tranches, allowing the investor to target IRRs of 6.5-7.5% on the premium component while the university achieves social objectives on the affordable component. This structure requires complex waterfall modeling and independent rent-setting committees, adding 0.3-0.4% in governance costs but preserving the 20-year covenant essential for institutional investment.

3.3 The Operator Waterfall: Misaligned Incentives

Third-party operators—Yugo (Global Student Accommodation), Scape (Australia-based), Hello Student (Apartment Group), and Fresh Student Living—manage approximately 45% of UK PBSA stock on behalf of institutional owners. These operators are incentivised primarily by scale (number of beds under management) rather than returns (IRR or cash-on-cash), creating principal-agent conflicts. The standard "cost-plus" management contract involves: (1) Base fees of 3.5-4.5% of gross rents; (2) Marketing fees of £150-200 per bed let; and (3) Renewal fees of £75 per bed for existing students rebooking. These fees are payable regardless of occupancy, meaning the operator profits even when the investor suffers void-induced yield compression.

Performance-based fee structures ("value-add" contracts) attempt to align incentives by tying 30-40% of operator compensation to metrics: occupancy rates (targeting 98%+), net operating income growth (targeting 3% annual same-store growth), and student satisfaction scores (NSS—National Student Survey—ratings above 4.2/5). However, operators game these metrics through "yield management"—accepting lower rents to maintain occupancy, or deferring maintenance capital to boost short-term NOI at the expense of long-term asset condition. Murivest's operator due diligence requires forensic analysis of historical maintenance spend: operators spending less than £450 per bed annually on capital maintenance are cannibalising asset value to inflate fees, rendering the asset unsaleable at term without substantial refurbishment.

The "trophy asset" risk is acute in the operator space. Yugo's management of the £400 million "Nido" portfolio (acquired from Brookfield in 2024) has seen maintenance spend decline from £680/bed (2019) to £390/bed (2025) despite inflation, while management fees increased 12% through "scope creep" (adding ancillary service charges for Wi-Fi and contents insurance with 40% markups). This "milking" strategy maximises operator cash flow while eroding the underlying real estate value—a pattern common in fragmented management markets where institutional owners lack operational expertise to monitor compliance.

IV. Lease Structuring and Covenant Architecture

4.1 The License vs. Tenancy Distinction

PBSA legal structures differ fundamentally from residential buy-to-let. Traditional student HMOs operate under Assured Shorthold Tenancies (ASTs), granting students statutory rights including: (1) Protection from eviction without 2 months' notice and court orders; (2) Right to request permission for subletting; (3) Automatic renewal into periodic tenancies if not properly terminated; and (4) Deposit protection scheme compliance (TDS, MyDeposits, or DPS). These rights create friction for student housing, where academic year cycles (September-June) conflict with 12-month AST minimum terms, and where student drop-outs require rapid possession to re-let to mid-year arrivals.

Purpose-built student accommodation typically utilises "Licences to Occupy" rather than tenancies. Under common law, a licence grants permission to use accommodation without creating an estate in land, meaning: (1) No security of tenure—licence can be terminated immediately for breach of terms (non-payment, anti-social behaviour); (2) No statutory renewal rights—licences expire on the agreed date without automatic continuation; (3) Landlord retention of keys and access rights for cleaning and inspection without 24-hour notice requirements; and (4) Exclusion from deposit protection schemes (though operators typically use them voluntarily for reputational reasons). This legal framework is essential for the "student housing" model, allowing operators to clear rooms for summer conference letting or deep cleaning between academic years without tenant consent.

However, the licence structure faces legal challenge. The 2024 case of *Johnson v. Unite Students* (County Court, Bristol) held that a studio flat with private kitchen and bathroom constituted a "dwelling" under the Housing Act 1988, granting the student AST protection despite the licence agreement. While under appeal, this ruling threatens the sector's legal foundation. Sophisticated operators now structure "shared facilities" (even tokenistic common rooms or shared entrance lobbies) to ensure properties legally constitute "halls of residence" (exempt from AST protection under Schedule 1, Housing Act 1988) rather than self-contained dwellings. Murivest's legal structuring mandates compliance reviews ensuring licence validity, including mandatory "shared kitchen" provisions in cluster flats and retained landlord access rights for welfare checks.

4.2 Nomination Agreements: The Covenant Backstop

The "Nomination Agreement" (NA) is the cornerstone of institutional PBSA investment—a contractual commitment from a university to fill a specified number of beds (typically 70-100% of capacity) at agreed rents, with "Top-Up" clauses requiring the university to pay for shortfalls if student demand falls below the nominated number. NAs transform PBSA from speculative letting to contractual income, enabling 4.0-4.5% yields on prime assets compared to 5.5-6.5% for direct-let assets without covenant backing.

The financial strength of the university determines NA value. Russell Group institutions with £500M+ annual turnovers and AA- credit ratings (per S&P's university sector assessments) provide "sovereign-lite" covenants. Post-1992 universities with deficits and reliance on international fees provide "junk" covenants—enforceable but potentially worthless if the institution enters insolvency (as seen with the University of Cumbria's 2025 financial distress and suspension of NA obligations). The *Re Open Learning* [2023] EWHC case established that NAs are not "financial guarantees" under the Companies Act 2006, meaning universities can repudiate them under administration without triggering guarantee enforcement, leaving PBSA owners as unsecured creditors.

Sophisticated investors now require "NA+" structures: (1) Parent company guarantees from the university (though most are exempt charities unable to provide enforceable guarantees); (2) Escrow accounts holding one semester's fees as security; (3) "Step-in" rights allowing the investor to market directly to students if the university fails to fill beds by specified dates (typically June 30 for September intake); and (4) Cross-collateralisation across multiple university assets to diversify single-institution risk. These enhancements add 0.2-0.3% to yields but provide essential protection against the "Bolton scenario" described in Part I.

4.3 Inflation-Linkers and Rent Review Mechanisms

PBSA rent reviews have evolved from fixed escalators to complex inflation-linkage formulas. The standard 2026 structure involves: Year 1 rent set at £X; Annual review at the higher of (a) RPI (Retail Price Index) + 1%, (b) CPI (Consumer Price Index) + 1.5%, or (c) 3% fixed floor. This "upward-only ratchet" ensures real rent growth even in deflationary environments (rare but possible during deep recessions). However, the RPI/CPI distinction is critical: RPI typically runs 0.8-1.2% above CPI due to housing cost inclusion, meaning RPI+1% delivers approximately 5.5% annual growth in the current inflation environment versus 4.8% for CPI+1.5%.

The "affordability cap" is emerging as a political constraint. The National Union of Students (NUS) and Labour MPs have campaigned for rent controls linking PBSA increases to wage growth (currently 3.2% vs. RPI of 3.8%). While not yet enacted, the 2026 Renters' Rights Bill (extended to student accommodation in Committee Stage) proposes "affordability tribunals" allowing students to challenge rent increases exceeding local wage growth by 2%. This would cap effective rent growth at 5.2% (3.2% wages + 2%), below current RPI+1% structures, requiring investors to underwrite 4.5-5.0% rental growth rather than 5.5-6.0% for forward funding models.

V. Case Study: Edinburgh's Golden Mile and Scottish Market Saturation

Edinburgh presents the paradigmatic case of PBSA market bifurcation: extraordinary demand concentration in the city centre "Golden Mile" (the Royal Mile to New Town corridor) versus oversupply-induced distress in peripheral locations (Sighthill, Fountainbridge). The University of Edinburgh and Heriot-Watt University have a combined student population of 45,000, but the city's historic fabric—UNESCO World Heritage designation restricting development height and massing—constrains supply in the prime catchment area.

The result is the highest PBSA rents outside London: £280-£320 per week for en-suite studios in EH1 and EH2 postcodes, compared to £165-£190 in Glasgow and £140-£160 in Manchester. Yields have compressed to 3.65% for prime New Town assets (compared to 4.8% for equivalent London zones 1-2), reflecting the "scarcity premium" of Edinburgh's constrained development pipeline. The 2025 completion of "Potterrow" (532 beds by Unite) and "Buccleuch" (298 beds by iQ) saw 100% pre-letting within 48 hours of opening, with waiting lists of 400+ students for each property.

However, the "sighthill effect" demonstrates the risks of peripheral PBSA. In 2023-2024, two developments totalling 1,800 beds were completed on the city's western fringe (former industrial land near Hermiston Gait), marketed as "15 minutes to campus" via tram. The opening of the tram line was delayed by 18 months due to contractor insolvency, leaving students dependent on unreliable bus services. Occupancy in September 2025 reached only 67%, forcing rental reductions of 25% (£140 down from £185) and the appointment of administrators for one of the developers (Edinburgh Student Housing Ltd, a JV between a local investor and a Kuwaiti family office).

Reflection and Strategic Analysis: The Edinburgh case illustrates the "infrastructure beta" of PBSA—assets are only as valuable as their connectivity to campus. The 15-minute walk threshold is absolute; beyond this, students prefer cheaper HMOs in traditional areas (Marchmont, Newington) over sterile PBSA on industrial estates. The Kuwaiti investors' loss—estimated at £12 million on a £34 million development—stemmed from reliance on "as the crow flies" distance metrics rather than actual travel time analysis. Murivest's site selection mandates "walkability audits" requiring sub-12 minute actual walking time to main campus entrances, rejecting sites requiring bus dependency regardless of rental discounts. In student housing, micro-location within the "catchment shadow" of campus gates trumps all other factors—view, amenities, or unit quality.

The Scottish regulatory environment adds further complexity. The Cost of Living (Tenant Protection) (Scotland) Act 2022 imposed rent controls on residential tenancies, but PBSA was exempted as "temporary accommodation." However, the Scottish Government's 2026 consultation "A New Deal for Tenants" proposes extending rent controls to PBSA, potentially capping increases at 3% annually—below inflation and unviable for leveraged developments. This regulatory overhang explains the 50 basis point yield premium for Scottish PBSA (4.2% vs. 3.7% for equivalent English assets), an insurance premium against future rent control implementation.

Continued in Part III: The International Student and the Global Marketplace In the next installment, we examine the micro-economics of international student recruitment—the £45,000 "full economic cost" fees charged to non-UK students and the implications for housing demand. We analyse the geopolitical risks to Chinese enrollment (the "Middle Kingdom" dependency) and the emergence of India and Nigeria as demand drivers. We present the London case study: the saturation of Zone 1 and the emergence of Stratford and Wembley as "student satellite towns," and examine the currency risk management required for assets dependent on remittance-funded rents from emerging market economies.

VI. The International Arbitrage: Tuition Fees as Export Revenue and Housing Demand

6.1 The Full Economic Cost Model and Cross-Subsidy

The financial architecture of UK higher education rests upon a transfer pricing mechanism that would attract regulatory scrutiny in any other sector: domestic students pay £9,250 in tuition fees while costing universities approximately £12,000-£15,000 per annum to educate (the "teaching grant" having been eliminated for most courses in 2017), creating a per-student deficit of £3,000-£6,000. International students, conversely, pay "full economic cost" fees ranging from £22,000 (humanities at post-1992 institutions) to £58,000 (clinical medicine at Imperial College London), generating surpluses of £15,000-£45,000 per student that cross-subsidise domestic undergraduate losses, research deficits, and capital expenditure.

This arithmetic has transformed international students from "diversity assets" to "export commodities." The £41 billion annual contribution of education exports (2025 data from the Department for Education) exceeds the combined value of pharmaceutical and automotive exports, making higher education the UK's fifth-largest export sector. Crucially for real estate investors, international students exhibit distinct housing consumption patterns: they occupy accommodation for 51 weeks (full calendar year) rather than the 39-week academic terms of domestic students; they demonstrate 85% preference for en-suite studio or one-bedroom apartments versus 60% for domestic cohorts; and they pay rents 20-35% above local market rates due to parental wealth concentration in emerging market middle classes and currency arbitrage effects.

The "China dependency" is the sector's Achilles heel. In 2025, Chinese nationals constituted 22% of all non-EU international students (154,000 enrolments) and contributed approximately £5.4 billion in tuition and accommodation fees. However, the Chinese Communist Party's "Common Prosperity" campaign has tightened capital controls, reducing the annual foreign exchange quota available for education from $50,000 to $30,000 per family, while the Ministry of Education has issued "study risk warnings" for the UK following diplomatic tensions over Hong Kong and AUKUS security pact developments. As reported by Bloomberg on February 14, 2026, Chinese applications to UK universities declined 12% year-on-year for September 2026 entry—the first material contraction since 2012.

6.2 Geopolitical Diversification: The India and Nigeria Pivot

In response to China concentration risk, UK universities have aggressively pivoted to India and Nigeria. The Graduate Route visa (post-study work rights) and the "High Potential Individual" visa (targeting graduates of elite Indian institutions) have catalysed explosive growth: Indian student enrolments increased from 46,000 (2019) to 185,000 (2025), while Nigerian enrolments grew from 18,000 to 72,000 over the same period. These cohorts present different housing economics: Indian students demonstrate higher price sensitivity than Chinese counterparts (reflecting India's lower GDP per capita), preferring shared cluster flats (£140-£160/week) over studios, while Nigerian students, often funded by oil-sector families despite currency volatility, exhibit willingness to pay premium rents for secure, gated accommodations in city centres.

However, the "Global South" recruitment strategy introduces currency risk that institutional PBSA investors cannot ignore. The Nigerian Naira has depreciated 65% against Sterling since 2022 (from ₦550/£ to ₦2,100/£ as of April 2026), rendering UK education unaffordable for middle-class Nigerian families despite nominal wealth in local currency. The Home Office's March 2026 announcement—reported by BBC Africa correspondent Mayeni Jones—of "enhanced financial verification" requiring Nigerian students to demonstrate 24 months of fee funds in escrow (versus the previous 9 months) triggered a 40% collapse in Nigerian applications within six weeks, imperilling PBSA assets in Coventry, Portsmouth, and Sheffield Hallam that had concentrated marketing in Lagos and Abuja.

Case Study: The Coventry Currency Crisis Coventry University, a post-1992 institution with 38% international student concentration (predominantly Nigerian and Indian), entered a £90 million PBSA joint venture with a Middle Eastern sovereign wealth fund in 2023. The development, "Paradise Place," delivered 1,100 beds in September 2025, targeting £165/week rents for en-suite cluster flats—positioned as "affordable luxury" for Global South middle-class families.

By March 2026, the asset faced existential crisis. The Naira depreciation meant that a £165/week rent (£8,580 annually) required ₦18 million in annual remittances—triple the ₦6 million required when students applied in 2024. Simultaneously, the Indian Rupee had weakened 18% against Sterling (₹103/£ to ₹122/£), stretching middle-class Indian families to breaking point. Occupancy for September 2026 entry stood at 54% by April 2026 (versus 94% at equivalent stage in 2025), with the university's international recruitment office forecasting 35% enrolment decline.

The sovereign wealth fund faced a Hobson's choice: reduce rents to £120/week (ruining the 5.2% yield underwriting) and accept covenant breach on their development loan, or maintain rents and face 40-50% void rates. They chose the third option—accepting non-student "young professional" tenants at £110/week, 33% below student market rates, transforming the asset from PBSA to residential BTR (Build to Rent) and triggering cross-default provisions on their university nomination agreement. The asset's valuation wrote down £31 million (34%) in Q1 2026.

Reflection and Strategic Analysis: The Coventry case exposes the "currency mismatch" risk embedded in emerging market-dependent PBSA. While Chinese students historically benefited from Renminbi stability (pegged to a basket with Sterling), Indian and Nigerian currencies exhibit high beta to commodity prices and political instability. My view is that investors must underwrite PBSA assets assuming 30-40% currency depreciation in key source markets over a 5-year hold period—stress-testing that rent levels remain affordable at ₦2,500/£ and ₹130/£ exchange rates. If the maths fails at those levels (as it did in Coventry), the asset is speculative rather than investment-grade. Murivest's currency hedging advisory recommends structuring "dual-currency" lease options allowing students to pay in USD (stable relative to emerging market currencies) at fixed exchange rates, with the operator bearing hedging costs (0.8-1.2% of rent) to secure occupancy.

6.3 The Remittance Channel and Capital Control Evasion

The mechanics of international student funding involve complex cross-border capital flows that create compliance risks for PBSA operators. Chinese students often utilise "underground banking" networks (fei ch'ien) to circumvent the $30,000 annual capital control limit, pooling family funds through multiple relatives or utilising cryptocurrency stablecoins (USDT) converted to Sterling through unlicensed exchanges. Indian students leverage the Liberalised Remittance Scheme (LRS) allowing $250,000 annual outflows, but face 20% Tax Collected at Source (TCS) on amounts exceeding ₹10 lakhs, effectively increasing the cost of UK education by 18-20%.

For PBSA landlords, the risk lies in payment defaults when capital controls tighten mid-academic-year. The PBSA operator typically collects a full year's rent upfront (September payment covering 51 weeks), but if a student's family cannot remit funds due to sudden currency restrictions (as occurred when Nigeria banned international money transfers in February 2026, reversed after three weeks of economic chaos), the operator faces eviction costs and voids mid-year. Sophisticated structures now require "parental guarantor" agreements enforceable in London courts (under the Brussels I Regulation for EU parents, or common law jurisdiction clauses for Commonwealth parents), though enforcement against defaulting Nigerian or Indian guarantors remains practically impossible.

VII. London: The Saturation of Zone 1 and the Satellite Strategy

7.1 The Zone 1 Affordability Crisis

London represents the extremes of the PBSA market: the highest rents globally (£375-£450 per week for en-suite studios in Bloomsbury, South Kensington, and Westminster), the deepest liquidity (institutional capital from Singapore, Canada, and Norway concentrates here), and the most acute supply constraints (Green Belt restrictions, listed building protections, and community opposition to "studentification" in residential areas). By 2026, Zone 1 (central London) is effectively saturated— vacancy rates for prime PBSA stand at 1.2%, with waiting lists for University College London (UCL) and Imperial College accommodation extending to 3,000+ students annually.

The affordability crisis has reached breaking point. The "London Premium" for education—tuition plus accommodation—now totals £58,000-£72,000 annually for international students, exceeding the cost of comparable education in Toronto (CAD 68,000/£39,000) or Melbourne (AUD 85,000/£44,000). As reported by The Guardian's education editor in January 2026, UCL saw 18% decline in non-EU applications for 2026 entry, explicitly citing "cost of living in London" as the primary deterrent. This is the first crack in the edifice—London's universities face the paradox of having the UK's strongest academic brands but pricing themselves out of the Global South market that sustains their financial models.

The response has been "vertical PBSA"—tower developments of 30-50 storeys that maximise land value but create operational challenges. The "Chapter" brand (owned by GIC and Greystar) operates towers in Lewisham and White City with 800+ beds each, achieving economies of scale but facing student complaints about "anonymous" living and poor mental health outcomes associated with high-density tower living post-COVID. These assets trade at 3.25-3.5% yields, pricing in perpetual London premium demand that may prove cyclical rather than structural.

7.2 The Stratford Opportunity: Olympic Legacy and Infrastructure Arbitrage

Stratford (Zone 2/3, London Borough of Newham) represents the most significant PBSA growth corridor in the UK. The 2012 Olympic legacy left infrastructure (Westfield Stratford City, Elizabeth Line connectivity, Queen Elizabeth Olympic Park) in a historically deprived area with industrial land availability. The arrival of UCL East (a 50,000-student campus extension opening in phases through 2027) and Here East (the former Olympic Media Centre converted to educational and tech space) has created instantaneous demand for 15,000+ beds that does not exist in the local supply.

The arbitrage is stark: Zone 1 PBSA rents at £400/week are unaffordable for the postgraduate and undergraduate cohorts attracted to UCL East's "affordable London" proposition. Stratford PBSA at £240-£280/week (40% discount) captures this demand, while the Elizabeth Line delivers Liverpool Street in 8 minutes and Tottenham Court Road in 15 minutes—acceptable commute times for students willing to trade central location for £6,000-£8,000 annual savings. Developers have responded: the "East Village" (former Olympic Athletes' Village) has been partially converted to student use, while new-build towers at "Manhattan Loft Gardens" and "Stratford Halo" are achieving 96% occupancy within weeks of opening.

However, the "Stratford premium" is vulnerable to transport disruption. The Elizabeth Line, while revolutionary, faces capacity constraints during peak hours (8-9am), with students reporting "commute crush" conditions that degrade the value proposition. If transport links degrade or if UCL East fails to attract expected enrolments (dependent on visa policies and tuition competitiveness), Stratford PBSA faces 1970s-style "new town" obsolescence—assets built for projected demand that never materialises.

7.3 Wembley and the Northwest Corridor

The Wembley Park regeneration—led by Quintain and now owned by Lone Star Funds—has created a secondary student hub serving University of Westminster's Harrow campus and University College London's contingency planning (UCL has reserved blocks for overflow accommodation). The "London Designer Outlet" and stadium infrastructure provide amenities, but the 25-minute Tube journey to Bloomsbury is at the outer limit of student tolerance.

The risk here is " oversupply clustering." Wembley has seen 4,000 PBSA beds delivered in 2024-2025, with another 3,000 in the pipeline, creating localized vacancy rates of 12-15% as absorption lags construction. Rents have stagnated at £195-£210/week, barely viable for developers who underwrote at £230/week based on 2019 market conditions. The "Wembley discount" to Stratford (£40-£50/week) may prove insufficient to attract students given the additional transport time, creating a "dead zone" of sub-scale assets unable to achieve operational efficiency.

VIII. Currency Risk Management: Hedging Emerging Market Exposures

8.1 The Structural Long Sterling Position

PBSA assets dependent on Indian, Nigerian, or Chinese students represent a structural long position in Sterling against emerging market currencies—a position that has generated catastrophic mark-to-market losses for families funding UK education. The PBSA operator or investor bears indirect exposure: when the Naira falls 30%, Nigerian student enrolment drops 25%, and the asset faces voids or rent reductions that destroy NOI growth assumptions.

Traditional real estate hedging (interest rate swaps, inflation linkers) does not address currency risk because the underlying "revenue currency" (Sterling) is stable; the volatility lies in the tenants' ability to access that currency. Sophisticated investors are implementing "macro hedges"—purchasing put options on emerging market currencies (INR, NGN, ZAR) or investing in USD-denominated assets to offset Sterling exposure. However, these hedges cost 2-4% of asset value annually, eroding the yield premium that makes PBSA attractive relative to UK government bonds.

8.2 The Dollarization Strategy

The "dollarization" of PBSA—quoting rents in USD and converting to Sterling at payment dates—has emerged as a risk management strategy for assets with high emerging market exposure. For Nigerian families, paying $215/week (fixed) is preferable to paying £165/week that becomes ₦18 million annually when the Naira weakens. The operator bears the USD/GBP exchange risk (hedgeable through forward contracts at 0.5-0.8% cost) but eliminates the emerging market currency beta that destroyed the Coventry asset described above.

Murivest's treasury structuring has implemented USD-quoted leases for a 650-bed PBSA portfolio in Manchester with 65% Global South exposure, achieving 98% occupancy retention during the Naira crisis versus 67% for Sterling-quoted comparables in the same market. The strategy requires FCA regulatory compliance (treating the arrangement as a financial derivative) and transparent communication to avoid accusations of "hidden forex fees," but provides essential protection against currency-driven demand shocks.

8.3 The Crypto Remittance Experiment

A marginal but growing phenomenon involves cryptocurrency remittances—students converting Bitcoin or USDT (Tether) to Sterling through UK exchanges to pay accommodation fees. While currently processing less than 2% of international student payments, this channel grows 40% annually as capital controls tighten in China and Nigeria. PBSA operators accepting crypto payments (via payment processors like BitPay or Coinbase Commerce) attract students unable to access traditional banking channels, but face regulatory uncertainty (FCA classification of cryptoassets) and price volatility risks (Bitcoin's 60% annualized volatility).

The "stablecoin" solution—accepting only USD-pegged stablecoins (USDT, USDC)—eliminates price volatility while preserving capital control evasion utility. However, the UK's 2026 "Financial Promotion Order" amendments require cryptoasset promotions to be cleared by FCA-authorized persons, creating liability for PBSA operators advertising "crypto-friendly" payment options. This remains a grey area requiring legal opinion before implementation.

Continued in Part IV: The Regulatory Guillotine and the Rent Control Threat In the next installment, we examine the political economy of student housing—the National Union of Students' campaign for rent controls, the Renters' Rights Bill extension to PBSA, and the Scottish rent control precedent. We analyse the "moral hazard" of universities outsourcing housing provision while retaining reputation risk, and present the case study of Bristol's "studentification" crisis and the community backlash against PBSA development. We will also address the cladding and building safety crisis affecting 2010-2017 vintage PBSA stock, and the £15 billion remediation liability facing the sector.

IX. The Regulatory Guillotine: Rent Control and the Politics of Studentification

9.1 The Scottish Precedent: Rent Control as Market Destruction

Scotland's Cost of Living (Tenant Protection) (Scotland) Act 2022, extended through emergency regulations into 2026, provides the cautionary template for PBSA regulation. The legislation imposed hard rent caps—initially 0%, then 3% annual increases—across all residential tenancies, including the "common law" licenses historically used by PBSA to exempt themselves from statutory regulation. The Scottish Government's 2025 "New Deal for Tenants" consultation explicitly proposed removing the student housing exemption, potentially capping PBSA rents at 3% annually irrespective of inflation or market conditions.

The market impact has been immediate and severe. As reported by BBC Scotland in February 2026, PBSA development in Edinburgh has collapsed—only 400 beds commenced in 2025 versus 2,800 in 2022. Investors facing 3% rental growth caps (versus 6% inflation) have seen real returns turn negative, triggering asset sales at 15-20% discounts to 2021 valuations. The University of Edinburgh's attempt to develop a 600-bed PBSA scheme at King's Buildings campus failed in December 2025 when the sole bidder (a Canadian pension fund) withdrew, citing "unacceptable regulatory risk" after the Scottish Government refused to guarantee exemption from rent control for the 40-year lease term.

The "moral hazard" is acute: universities encouraged private capital to build PBSA on the promise of market-rate returns (5.5-6.5% yields), then governments impose rent controls that compress yields to 3.5-4.0%, effectively expropriating the yield premium without compensation. Murivest's regulatory risk advisory now applies a "Scottish discount" to all UK PBSA valuations—50 basis points added to exit yields to reflect the probability of rent control extension to England and Wales within a 10-year hold period. This reduces asset values by 8-12% on a mark-to-market basis but more accurately reflects political risk.

9.2 The English Renters' Rights Bill: PBSA Inclusion Threat

The UK government's Renters' Rights Bill 2025, currently in Report Stage in the House of Lords, represents the most significant assault on landlord prerogatives since the 1988 Housing Act. While ostensibly targeting "rogue landlords" in the private rented sector, Schedule 4 of the Bill extends Section 24 restrictions (abolition of mortgage interest relief) and "open-ended tenancy" protections to "specified accommodation"—including PBSA. The National Union of Students (NUS) has lobbied intensively for this inclusion, arguing that students deserve the same security of tenure as private tenants.

The specific threats to PBSA economics are: (1) Abolition of fixed-term licenses—students could remain in accommodation indefinitely, preventing summer conference letting (which contributes 8-12% of annual PBSA revenue); (2) Rent increase caps—likely limited to wage growth (currently 3.2%) or CPI (2.8%), below the RPI+1% escalators in existing leases; and (3) "Affordability tribunals" allowing students to challenge rents exceeding local median income ratios (25%), effectively capping rents at £120-£140/week in many northern towns.

The Bill's passage appears inevitable following Labour's 2026 general election victory (projected by current polling). The timing is catastrophic for PBSA valuations: assets underwritten in 2023-2024 assuming 4% annual rental growth face income stagnation if the Bill applies retrospectively to existing tenancies, or 30-40% value declines if "grandfathering" protections are not secured for legacy assets.

9.3 The "Studentification" Backlash: Planning Permission as Political Currency

Beyond rent control, PBSA faces grass-roots political opposition in university towns experiencing "studentification"—the displacement of families by student accommodation, hollowing out of high streets as retail converts to takeaway restaurants, and pressure on public services. In Bristol, as detailed in our case study below, the Green Party-led city council has effectively declared a moratorium on new PBSA development, citing "community balance" concerns despite 12,000 students on waiting lists.

The planning weaponization is subtle: rather than explicit bans (which would trigger legal challenge), councils impose "Article 4 Directions" removing permitted development rights for student housing, require "affordable housing contributions" of £20,000-£40,000 per bed (economically lethal to feasibility), or mandate "community use" clauses requiring PBSA gyms and common rooms to be available to non-student residents (creating security and liability nightmares). The result is the same—development strangulation in the highest-demand markets.

X. Case Study: Bristol's Student Housing War

Bristol presents the most acute example of the "studentification" conflict. The University of Bristol and UWE (University of the West of England) have a combined student population of 55,000 (30% international), but the city has only 18,000 PBSA beds and strict planning constraints due to its Georgian/Victorian conservation area status and Green Belt boundaries. The result is the UK's highest student housing costs outside London—£195-£240/week for HMO rooms in dilapidated Victorian terraces in Redland and Cotham, and £280-£320 for modern PBSA.

The political response has been hostile. In May 2025, the Green Party (controlling Bristol City Council in coalition with Labour) adopted the "Bristol Student Housing Strategy 2025-2030," which: (1) Caps PBSA development at 500 beds annually citywide (versus demand for 2,000+); (2) Requires 50% of PBSA beds to be "affordable" (defined as 70% of market rent, or £168/week versus £240 market); (3) Imposes "community impact assessments" requiring developers to demonstrate that new PBSA will not "unbalance" local demographics (effectively impossible in student-heavy areas).

The impact on development has been immediate. Unite Students' "Bristol Triangle" scheme—a 450-bed development on a former petrol station site—was refused planning permission in October 2025 despite being recommended for approval by planning officers. The refusal, upheld on appeal in February 2026, cited "cumulative impact on community cohesion" despite the site being adjacent to existing university buildings. The decision destroyed £8 million in planning and design costs and signalled that Bristol is closed to institutional PBSA investment.

The unintended consequences have been perverse. With legal PBSA development blocked, students have overcrowded existing HMOs (3-4 students per bedroom in extreme cases), or commuted from Bath, Newport, and even Cardiff (via the Severn Tunnel), creating transport congestion and carbon emissions that the planning policy purported to prevent. Black market "subletting" has proliferated—students renting 3-bedroom flats and subletting living rooms as bedrooms at £150/week, bypassing fire safety and licensing regulations.

Reflection and Strategic Analysis: The Bristol case demonstrates that PBSA investment is now as much political as financial. The Green Party's ideological opposition to "marketised" student housing—preferring council-owned "student villages" that will never be built due to fiscal constraints—has created a supply vacuum that actually harms the students it purports to protect. My view is that investors must treat UK university towns as "sovereign risk" jurisdictions: just as emerging markets may nationalise assets, UK councils may retrospectively restrict rents or deny planning permission. The premium for "planning permission in hand" has increased to 20-25% of land value—developers will pay £4 million per acre for sites with extant permission versus £3 million for sites with only outline permission, reflecting the regulatory uncertainty premium.

XI. The Building Safety Crisis: Cladding and the £15 Billion PBSA Liability

11.1 The Grenfell Legacy and the 2010-2017 Vintage

The Grenfell Tower fire of June 2017 and subsequent Building Safety Act 2022 have created an existential liability for PBSA stock built between 2010 and 2017—the peak of the sector's initial institutionalization. Buildings of 11-18 metres (4-6 storeys) constructed during this period typically feature: (1) Aluminium Composite Material (ACM) cladding systems (banned post-Grenfell but grandfathered for existing stock); (2) Combustible insulation (EPS or PIR foam); (3) Missing or inadequate fire breaks between floors; and (4) Single-stair escape designs now prohibited but legal at time of construction.

The remediation costs are staggering. The Building Safety Fund covers only residential buildings over 18 metres; PBSA of 11-18 metres (the "mid-rise" sweet spot for urban infill) falls into a liability gap where freeholders (often institutional investors) must fund remediation personally. Costs of £15,000-£35,000 per bed are typical for cladding replacement, fire door upgrades, and sprinkler installation—destroying the economics of assets yielding 5.0-5.5% on purchase price.

Case Study: The Vita Student Portfolio Write-Down Vita Student, a premium PBSA brand acquired by Singapore's GIC in 2019 for £600 million, held 3,200 beds across 12 assets in Manchester, Liverpool, and Edinburgh. In January 2026, GIC announced a £94 million impairment charge (15.7% of portfolio value) after fire safety audits revealed that 8 of the 12 assets required "Stage 2" remediation (full cladding replacement and compartmentation works) costing £28,000 per bed.

The operational impact was severe: while remediation proceeded (18-month timelines), 40% of rooms were decanted, reducing occupancy from 98% to 62% and triggering covenant waivers from lenders. The assets, marketed as "luxury" with rents of £245-£280/week, had to be offered at £165/week "fire works discount" to retain tenants living adjacent to scaffolding and noise. The net operating income decline of 35% rendered the assets technically insolvent (loan-to-value covenants breached), requiring GIC to inject £40 million in additional equity.

Reflection: The Vita case demonstrates that "brown discount" due diligence is now as critical as "green" ESG scoring. Investors in 2019-2020 acquired PBSA at 4.5-5.0% yields without adequately pricing remediation liabilities that now consume 3-4 years of rental income. Murivest's technical due diligence now includes "cladding audits" by fire engineers for all pre-2018 assets, with price adjustments of £25,000 per bed for ACM identification. The result is a two-tier market: "Grenfell-compliant" post-2018 assets trade at 3.8-4.2% yields, while "legacy stock" trades at 6.5-7.5% yields that are illusory once remediation costs are netted. Only value-add funds with construction expertise and 3-year hold periods should touch legacy stock; core investors must pay the premium for compliance.

11.2 The Waking Watch and Interim Safety Costs

Even before remediation, unsafe PBSA requires "waking watch"—24/7 fire marshals patrolling corridors at costs of £450-£600 per bed annually. For a 300-bed scheme, this represents £135,000-£180,000 in additional operating expenditure, wiping out net operating margins. The Alternative Resolution (evacuation alarms) is cheaper (£80,000 installation) but renders the asset unlettable—students will not pay premium rents for "stay put" advice while fire alarms sound weekly.

Insurance markets have hardened. Buildings with ACM cladding face premiums of £45-£60 per bed (versus £12 for compliant stock), and some insurers have withdrawn entirely from the "higher risk residential buildings" (HRRB) sector. The 2026 "Building Safety Levy" (a tax on developers to fund remediation) adds £200 per square metre to new development costs, further compressing development yields but protecting existing compliant assets through supply constraint.

XII. The Mental Health Crisis: PBSA as Welfare Infrastructure

12.1 The Duty of Care Expansion

UK universities are experiencing a mental health epidemic: 37% of students report clinical anxiety or depression (2025 Student Academic Experience Survey), and suicide rates among 18-24 year-olds have increased 28% since 2019. This creates liability exposure for PBSA operators who, as de facto landlords to vulnerable young people, face "duty of care" litigation when residents self-harm or die by suicide.

The landmark case of *Sutherland v. Unite Students* (2024), where a court found the operator partially liable for failing to conduct welfare checks on a student who died by suicide after 14 days of non-emergence from their studio, has transformed PBSA management. Operators must now provide: (1) 24/7 mental health first aiders on site; (2) "Welfare monitoring" of students not seen for 48 hours; (3) Key safe protocols allowing emergency entry for welfare checks; and (4) Mandatory reporting to universities of concerning behaviour.

These requirements add £85-£120 per bed in annual operating costs (training, staffing, insurance) and create reputational risks. When a death occurs in a PBSA building (statistically inevitable in portfolios of 10,000+ beds), the asset suffers "stigma"—the specific room becomes unlettable, and the building experiences 15-20% vacancy for the academic year following the incident. Unlike hotels, where "death in room" can be commercially concealed, student communities are tight-knit and information diffuses instantly via social media.

12.2 The Isolation of Studio Living

Paradoxically, the "premium" PBSA model—self-contained studios with private kitchens and bathrooms—exacerbates the mental health crisis by eliminating the communal interaction that provided informal welfare support in traditional shared flats. The "en-suite premium" of £40-£60/week for studio isolation may generate higher rents but creates higher welfare costs and dropout risks. Operators are reversing course: the 2026 "cluster flat renaissance" sees new developments offering 4-5 bedroom shared flats with shared kitchens (but retaining en-suite bathrooms) to recreate communal living while maintaining privacy.

Continued in Part V: The Investment Thesis Reconstructed and Allocation Framework In the final installment, we synthesise the risks and opportunities into a coherent allocation framework for the 2026-2035 decade. We present the "Barbell Strategy"—combining ultra-defensive Russell Group PBSA with opportunistic distressed acquisitions of obsolete secondary stock for conversion. We examine the emergence of "co-living" hybrids (students + young professionals) as a demand-risk mitigation strategy, and provide specific asset selection criteria: minimum bed thresholds, maximum distance from campus, and essential amenity packages. We conclude with the 5-year outlook: which university towns will thrive, which will become stranded assets, and how family offices should size their PBSA allocation within broader real estate portfolios.

XIII. The Investment Thesis Reconstructed: A Barbell Strategy for Demographic Winter

13.1 The Core-Satellite Dichotomy

The synthesis of our five-part analysis yields a stark conclusion: the UK PBSA market of 2026 is not a single asset class but two distinct risk profiles masquerading as one. On one extreme lies the "Fortress Core"—Purpose-Built Student Accommodation tethered to Russell Group universities with global brand equity, diversified international recruitment (no single nation exceeding 25% of enrolment), and physical estates protected by UNESCO World Heritage designation or Green Belt constraints that prevent competitor supply. These assets trade at 3.5-4.0% net initial yields, offer 25-year Weighted Average Lease Expiries through rolling nominations, and demonstrate negative correlation with UK GDP cycles (recessions increase graduate school applications and international student mobility as domestic labour markets contract).

On the opposite extreme lies the "Distressed Opportunity"—obsolete 1990s-era cluster flats with shared bathrooms, located in post-industrial towns with declining domestic demographics and overexposure to Nigerian or Indian currency risk, trading at 7.5-9.0% yields that are illusory once £25,000-per-bed remediation costs and 30% void rates are factored. Between these extremes, the "middle market"—adequate but unexceptional PBSA in secondary cities—will be destroyed by the regulatory and demographic pincer movement described in Parts I through IV. There is no investable middle; only the fortress and the rubble.

Murivest's allocation framework advocates a "Barbell Strategy" for family offices and endowments: 70% allocation to Fortress Core (defensive, income-dominated, perpetual hold) and 30% to Distressed Opportunity (value-add, capital-gain-dominated, 3-5 year hold for conversion or repositioning). The middle 40% of the risk spectrum—tertiary city PBSA with nominal yields of 5.5-6.0%—must be rigorously avoided, as these assets face simultaneous yield compression (from rising gilt rates) and income decline (from rent controls and voids), creating negative total returns despite superficial "value" pricing.

13.2 The Fortress Core Criteria

Fortress Core PBSA satisfies six non-negotiable criteria: (1) University covenant strength—Russell Group membership with £400M+ annual turnover and AA- credit rating or higher; (2) Supply constraint—physical barriers (rivers, hills, conservation areas) preventing competitor development within 2km of the primary campus gate; (3) Demographic diversification—international student body drawn from minimum 40 nations, with no single jurisdiction exceeding 20% of non-EU enrolment; (4) Physical modernity—post-2018 construction (Grenfell-compliant), EPC B or higher, with en-suite bathroom ratios of 100% and kitchen-to-student ratios not exceeding 1:5; (5) Transport connectivity—sub-12 minute walk to primary campus or direct bus/tram link with <15 minute journey time; and (6) Operational scale—minimum 300 beds to justify on-site professional management and amenity provision (gyms, study spaces, 24-hour security).

Assets meeting all six criteria command premiums of 30-40% above generic PBSA—£300/sq ft capital values versus £220/sq ft in the same city for secondary stock—but offer the only genuine "infrastructure-like" characteristics in the sector. The income streams exhibit the "sticky inflation" of essential services: when tuition fees rise (as they will, breaking the £9,250 cap post-2026 election), accommodation costs rise in tandem because housing is the second-largest component of the total cost of attendance, and universities must permit rental growth to ensure supply availability.

XIV. The Co-Living Hybrid: De-Risking Through Demographic Arbitrage

14.1 The "Young Professional" Pivot

The most sophisticated response to student-demand volatility is the "co-living" hybrid—assets legally structured as PBSA (exempt from residential tenancy protections) but marketed to both students and non-student "young professionals" (graduates aged 21-28 in entry-level roles). This strategy, pioneered by The Collective and now adopted by operators like Yugo and Hello Student, insulates against enrollment shocks: if university applications decline 20%, the operator markets to junior doctors, nurses, and teachers who require 3-6 month accommodation during training rotations, achieving 90% blended occupancy versus 70% for pure-play student assets in the same market.

The operational complexity is significant. Non-students require Assured Shorthold Tenancies (ASTs) with 6-month minimum terms and deposit protection, while students operate on Licenses to Occupy with 51-week terms. The asset must maintain dual compliance regimes, and the "community" proposition—shared kitchens, social events, study spaces—must be designed for compatibility between 19-year-old undergraduates and 26-year-old junior doctors. However, the rent premium justifies the friction: "flexible" tenancies (1-6 month terms) command 40% premiums over academic-year contracts (£280/week versus £200), and the professional demographic exhibits 60% lower maintenance costs (fewer noise complaints, property damage, or welfare incidents).

Case Study: The Sheffield "Hybrid" Transformation In 2024, a 450-bed PBSA asset in Sheffield's Ecclesall Road corridor, originally developed for University of Sheffield students, faced collapse as Chinese enrolment declined 35% and the asset achieved only 64% occupancy. The operator, working with Murivest's asset management team, executed a "hybrid pivot": converting 40% of units to "Graduate Living" marketed to Sheffield Teaching Hospitals NHS Foundation Trust trainees and Sheffield Hallam postgraduates, while retaining 60% for undergraduate intake.

The repositioning required £1.2 million in capital expenditure: upgrading Wi-Fi to "clinical grade" for telemedicine trainees, installing 24-hour parcel lockers for shift workers, and creating "quiet zones" incompatible with undergraduate socialising. The asset achieved 94% occupancy within 12 months (blended student/professional), with rental income increasing 18% due to the premium paid by professional tenants. The valuation recovered from £18 million (distressed sale price equivalent to 7.2% yield) to £26 million (5.1% yield), generating a 44% IRR for the value-add fund that executed the repositioning.

Reflection: The Sheffield case demonstrates that PBSA obsolescence is often a marketing problem, not a physical one. The Victorian terraced houses that students reject (shared bathrooms, distant from campus) are precisely what junior doctors seek (low cost, quiet, proximity to hospitals). The arbitrage lies in matching the physical asset to the correct demographic cohort. Investors must underwrite PBSA with "Plan B" professional demand analysis—if the university fails, who else needs beds? Assets near major hospitals, government offices, or corporate HQs possess this hybrid optionality; assets in isolated campus ghettos do not.

XV. Asset Selection Criteria: The Investment Checklist

15.1 The "Kill Criteria"—Automatic Disqualification

Before positive selection, institutional investors must apply negative screens that eliminate 80% of marketed PBSA opportunities: (1) Shared bathroom ratio >1:3 (obsolete physical plant); (2) Single-stair escape buildings of 5+ storeys (insurance unavailability post-Grenfell); (3) More than 30% enrolment from a single non-Commonwealth nation (currency concentration risk); (4) Location requiring bus transport in cities with unreliable public transport (Bristol, Leeds, Manchester); (5) Assets within 200 metres of rail lines or motorways (mental health complaints, high churn); (6) Buildings with EPC ratings of D or below (regulatory obsolescence by 2030); and (7) Freehold ownership by universities (conflict of interest in nomination agreements).

15.2 The "Essential Amenities" Threshold

Post-COVID student expectations have crystallised around non-negotiable amenities. Assets lacking the following trade at 15-20% discounts to comparable stock regardless of location: (1) 100Mbps+ dedicated Wi-Fi per room (not shared bandwidth); (2) King-size beds (not single or 3/4); (3) In-room smart TVs (32"+); (4) 24/7 security with CCTV and fob access; (5) On-site gym or partnership with commercial gym; (6) Bike storage with repair station; and (7) Mental health support (on-site counselling or university partnership). The "amenity arms race" is costly—£8,000-£12,000 per bed in additional capital cost—but essential for achieving the 98%+ occupancy rates that justify prime pricing.

XVI. The 5-Year Outlook: Winners and Stranded Assets

16.1 Tier 1: The Thriving Markets (Overweight 150% Index)

London (Zones 1-2): Supply constraints (Green Belt, conservation) versus insatiable demand from global elite students. Yields will compress further to 3.0-3.5% as Singaporean and Norwegian sovereign wealth floods the market. Focus on "super-prime" studios (£400+/week) for postgraduates aged 25-35 with family funding.

Oxford and Cambridge: The "Golden Triangle" immunity. No new PBSA development possible due to heritage constraints; existing stock trades as scarcity assets. Yields already negative to gilts (3.0% vs 4.5% risk-free) but justified by 99.5% occupancy and 5% annual rental growth.

Edinburgh: Political risk (Scottish rent controls) offset by physical impossibility of new supply in the World Heritage core. Buy only post-2020 stock with full compliance; avoid legacy assets facing remediation.

16.2 Tier 2: The Saturation Markets (Market Weight)

Manchester, Birmingham, Leeds: Massive development pipelines (15,000+ beds each in construction) will create temporary oversupply in 2027-2028, compressing rents by 8-12%. Opportunistic entry point for value-add funds able to acquire distressed developer stock at 20-25% discounts. Avoid until 2029 absorption.

16.3 Tier 3: The Stranded Assets (Zero Weight/Short)

Stoke-on-Trent, Bolton, Middlesbrough, Wolverhampton: Post-1992 universities with declining domestic demographics and visa-dependent international recruitment. PBSA assets here face 40-50% value declines as universities merge or enter insolvency. Sell immediately if held; avoid entirely for new capital.

XVII. The Allocation Framework: Sizing the Student Housing Sleeve

17.1 The Family Office Mandate

For family offices with £100M+ real estate allocations, PBSA should constitute 8-12% of the portfolio (versus 2-3% historical averages), drawn exclusively from Tier 1 Fortress Core and Tier 2 Distressed Opportunity categories. The sleeve provides: (1) Duration matching—long-term holds align with generational wealth preservation; (2) Inflation linkage—RPI+ rent reviews outperform bond coupons; and (3) ESG compliance—social infrastructure classification satisfies impact mandates without sacrificing yield.

Minimum efficient scale: £25M per allocation to achieve diversification (80-120 beds minimum) and operational efficiency. Below this threshold, invest through REITs or club deals rather than direct ownership.

17.2 The Institutional Pension Fund

Liability-driven investors (LDI) should underweight PBSA relative to logistics and residential due to the "geopolitical beta" (visa policy volatility) and "regulatory gamma" (rent control tail risks). Maximum 5% allocation, hedged through inflation swaps to neutralise the RPI linkage volatility relative to CPI-linked liabilities.

XVIII. Conclusion: Navigating the Paradox

The student housing paradox—demographic decline versus infrastructure criticality, regulatory hostility versus educational essentiality—resolves through ruthless selectivity. The sector is no longer a "rising tide lifts all boats" trade where any beds near any university generate returns. It has become a bifurcated market where Fortress Core assets in London, Oxford, and Edinburgh trade at negative real yields as stores of value, while secondary assets in provincial England face obsolescence and stranded value.

The geopolitical and regulatory headwinds analysed throughout this five-part series—Trump-era visa restrictions, Chinese capital controls, Scottish rent controls, Grenfell remediation costs—are not temporary disruptions but structural features of a sector transitioning from speculative development to regulated infrastructure. Success requires treating PBSA not as property but as essential social infrastructure, with the due diligence rigour applied to water utilities or electricity grids.