Breaking News

Kenya’s PSV Fuel Strike and the Commercial Real Estate Fragility Question

Kenya’s PSV Fuel Strike and the Commercial Real Estate Fragility Question

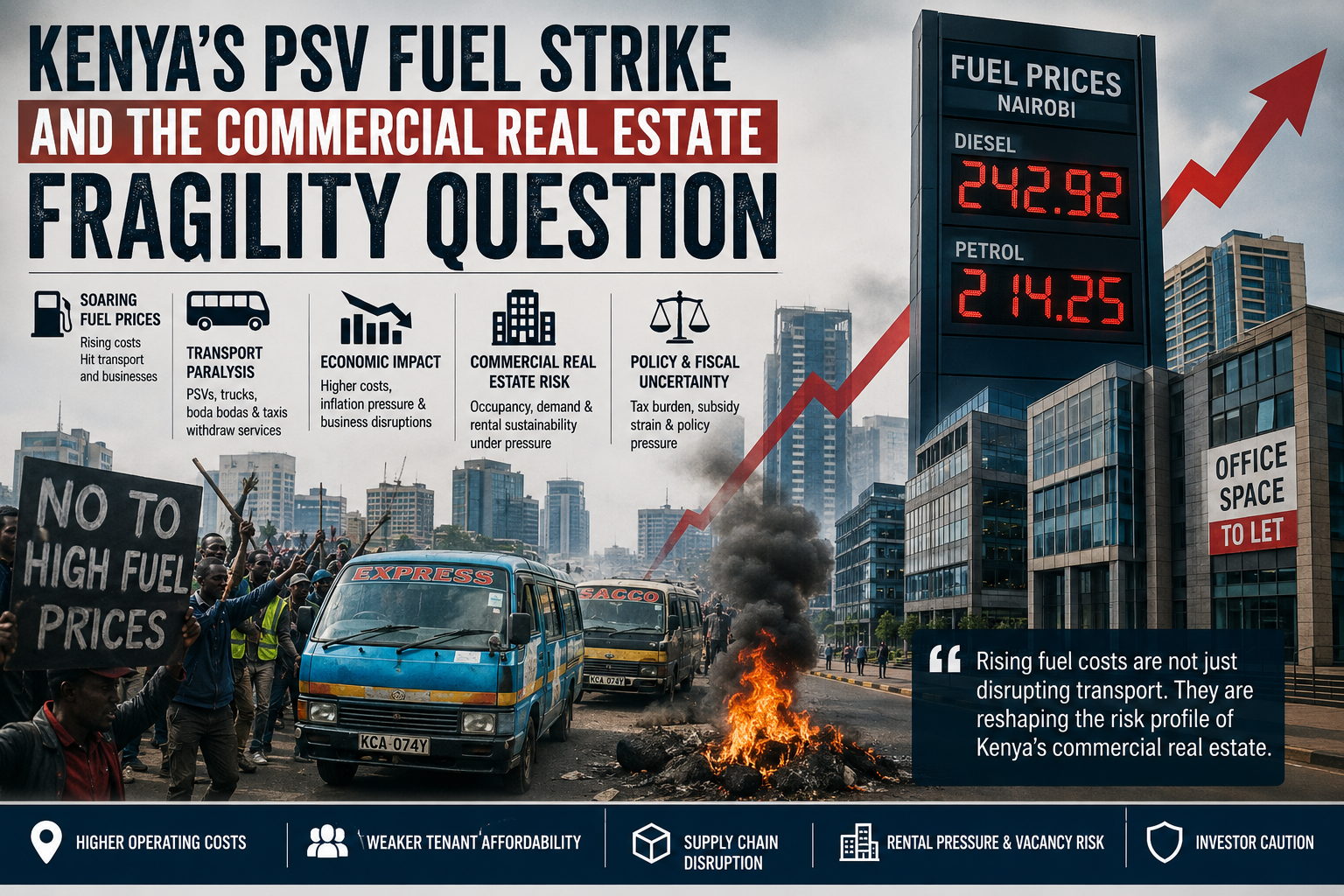

Kenya’s nationwide public service vehicle strike has exposed a deeper economic reality extending far beyond commuter disruption. The protests, triggered by sharp increases in diesel and petrol prices, revealed how tightly Nairobi’s commercial real estate ecosystem remains connected to transport economics, logistics efficiency, and fuel-dependent urban infrastructure.

For institutional property investors, the more important observation is not the temporary transport paralysis itself. It is the structural vulnerability the disruption exposed. Rising diesel costs are increasingly influencing logistics pricing, industrial operating margins, commuter-driven retail demand, and office market occupancy dynamics across Nairobi and major urban corridors.

Transport Economics Now Directly Influence Commercial Property Performance

Commercial real estate markets do not operate independently from infrastructure systems. In Kenya, the relationship is particularly pronounced because logistics, labour mobility, and urban commuting remain heavily road-dependent.

The latest EPRA pricing adjustments pushed Nairobi diesel prices above Ksh.230 per litre even after revisions, materially increasing transport costs for logistics operators, retailers, manufacturers, and industrial occupiers. Distribution margins compress quickly when diesel pricing accelerates faster than consumer purchasing power.

Industrial landlords across Mombasa Road, Athi River, ICD, and emerging logistics corridors increasingly face tenant conversations centered not simply on rent, but on operating efficiency. Fuel inflation changes tenant behavior. Occupiers prioritize proximity to highways, labour pools, and distribution centres more aggressively during periods of transport stress.

Historically, Nairobi commercial property analysis focused heavily on location prestige and nominal yield spreads. The next cycle may increasingly reward logistical efficiency instead.

The Nairobi Office Market Faces a Different Kind of Pressure

Office markets typically weaken through oversupply, economic contraction, or financing stress. Kenya’s current environment introduces another pressure point: commuter fragility.

Nairobi’s urban workforce remains heavily dependent on privately operated matatu systems and boda boda connectivity. When transport costs spike abruptly, commuting becomes economically punitive for middle-income workers. That dynamic influences attendance behavior, hybrid work adoption, and eventually corporate space optimization decisions.

Grade A office markets in Westlands, Upper Hill, Kilimani, and parts of Riverside already face competitive pressure from changing workplace models. Persistent transport volatility may accelerate tenant preference toward mixed-use environments where residential, retail, and office functions sit closer together.

In contrast, mature gateway markets such as Dubai and selected European cities benefit from more integrated transport systems with broader energy diversification and institutional transit support. Nairobi remains more operationally exposed to fuel-linked disruption cycles.

Industrial Logistics Assets Could Emerge Stronger Long Term

Paradoxically, periods of operational disruption often clarify which real estate segments possess structural resilience.

Kenya’s industrial and logistics sectors continue benefiting from long-duration fundamentals including population growth, regional trade integration, e-commerce penetration, and East African supply-chain expansion. However, the strike reinforces a growing divide between strategically located logistics assets and secondary industrial stock lacking infrastructure efficiency.

Institutional occupiers increasingly evaluate route optimization, fuel sensitivity, labour accessibility, and turnaround efficiency as part of broader real estate decision-making. Warehouses positioned closer to major highways, dry ports, labour catchments, and distribution nodes may continue commanding stronger occupancy durability despite macroeconomic volatility.

This partially mirrors trends observed in US logistics corridors following supply-chain disruptions after 2020. In both cases, investors increasingly value operational resilience over purely speculative appreciation narratives.

The Real Issue Is Institutional Confidence and Capital Allocation

Short-term strikes rarely determine long-term property cycles on their own. Institutional investors instead evaluate what disruptions reveal about governance capacity, infrastructure resilience, and policy predictability.

The Kenyan government’s rapid response — including emergency meetings between Treasury, Energy, and Transport stakeholders — reflects recognition that fuel pricing now carries wider macroeconomic implications extending beyond household inflation.

Commercial property investors monitor these dynamics closely because operating-cost instability can materially influence tenant affordability, absorption velocity, and underwriting assumptions. Markets experiencing unpredictable transport shocks often require higher risk premiums from long-duration capital allocators.

Yet there is another side to the equation. Markets with temporary volatility frequently create pricing inefficiencies. Sophisticated allocators sometimes increase exposure during periods of uncertainty when underlying demographic and urbanization fundamentals remain intact.

Where the Risks Still Sit

Kenya’s commercial real estate sector remains fundamentally attractive over the long term, but several vulnerabilities deserve careful consideration.

Fuel inflation introduces sustained operating pressure across logistics networks, manufacturing activity, and commuter-linked retail systems. If transport costs continue rising faster than income growth, tenant affordability may weaken in secondary office and retail segments.

There is also fiscal risk. Government revenue pressures limit room for prolonged subsidy interventions or aggressive tax relief. That creates uncertainty around future energy pricing stability and infrastructure funding capacity.

Investors should also distinguish between prime institutional assets and weaker secondary inventory. During periods of economic stress, capital typically concentrates toward better-located assets with stronger tenant profiles and infrastructure connectivity.

None of this eliminates Kenya’s long-duration growth story. But it reinforces the importance of disciplined asset selection and infrastructure-aware underwriting.

Portfolio Strategy Takeaway

Kenya’s PSV fuel strike should not be interpreted merely as a temporary transport dispute. It represents a broader signal regarding how infrastructure dependence, operating costs, and urban mobility increasingly shape commercial real estate performance.

For sophisticated investors and family offices, the strategic implication is clear. Future commercial property outperformance in Nairobi is likely to depend less on speculative appreciation narratives and more on operational resilience, infrastructure positioning, and logistics efficiency.

In practical terms, this favours industrial corridors with strong transport connectivity, mixed-use developments reducing commuter dependency, and institutional-grade commercial assets capable of maintaining occupancy stability during periods of macroeconomic stress.

Frequently Asked Questions

Why does a fuel strike matter for commercial real estate investors?

Fuel price shocks directly affect logistics efficiency, tenant operating costs, commuter flows, and distribution economics. Industrial and logistics properties are particularly sensitive because transport costs materially influence occupancy demand and profitability.

Which Nairobi commercial property sectors are most exposed to fuel volatility?

Industrial logistics corridors along Mombasa Road, ICD-linked warehousing, commuter-driven retail centres, and transport-dependent office submarkets face the highest operational sensitivity during fuel disruptions.

Could persistent fuel inflation alter institutional allocation strategies in Kenya?

Yes. Persistent fuel inflation tends to shift institutional demand toward logistics-efficient developments, mixed-use assets, and strategically located industrial properties closer to labour and distribution catchment zones.

How does Nairobi compare with mature international commercial property markets?

Unlike London or Dubai, Nairobi remains highly dependent on diesel-linked public transport systems and road-based logistics infrastructure. This creates greater short-term operational volatility during energy shocks but also creates selective pricing inefficiencies for long-term investors.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All commercial real estate acquisition decisions should be made with independent professional guidance. Murivest Realty Group Ltd is an independent real estate advisory firm. We do not act as a licensed investment advisor and do not offer regulated financial products or collective investment schemes. We do not pool capital from multiple investors. All advisory engagements are mandate-based, subject to formal documentation, comprehensive KYC/AML verification, and explicit scope definition. No investment decisions should be made based on information contained in our materials without independent verification, professional legal counsel, and comprehensive due diligence. Past advisory outcomes do not guarantee future results. All investments carry inherent risks, including potential capital loss.

Filed under

Related Reading

Breaking News

Kenya Fuel Crisis Latest: How Record Pump Prices and PSV Strikes Are Forcing a Commercial Real Estate Repricing

10 min read

Affordable Housing

Kenya's Affordable Housing: Progress, Challenges, and Your Role as an Investor

6 min read

Investment

Diani and Watamu Land have appreciated by 400% since 2020

9 min read

Murivest Community

Investor Discussion

Discuss investment opportunities, market trends, lease activity, financing, and underwriting with the Murivest community.

Join the Discussion

Share investment insights, market commentary, or leasing observations.

Professional discussion only. All comments are moderated.

Loading…

No discussion yet — be the first to contribute an insight.

Ask Murivest Research

Submit a Research Question

Questions on underwriting, leasing, market fundamentals, or capital structures are answered by the Murivest desk.

Murivest Research